Be prepared as rates are going up more in 2022 and likely in 2023 too

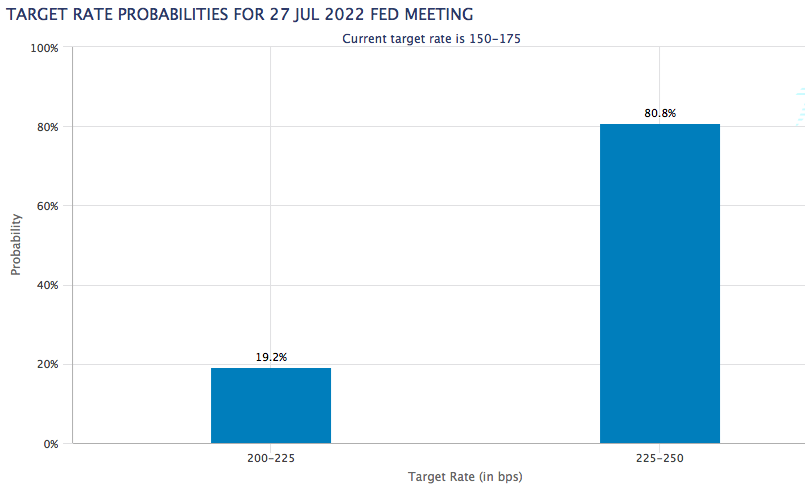

A few days before the beginning of August 2022, Wall Street’s eyes and ears were on the Federal Reserve, and as expected, the FOMC raised the fed funds rate by 75 basis-points. It was the Fed’s second consecutive 75 basis-point increase, taking its benchmark rate to a range of 2.25%-2.5%.

But what was surprising, at least to some, was that the Fed seemed to signal that the pace of rate hikes might slow down in 2022, as Fed Chair Jerome Powell said there will be a point where the Fed starts to slow hikes to assess their impact.

As an investor, you undoubtedly ask when, or if, the Federal Reserve Bank raises interest rates, how will that affect consumers and businesses? In particular, what about the consequences for certain segments of the economy?

Reason for the Fed’s Change

The most important tool available to the Fed is its ability to set the federal funds rate, or the prime interest rate. This is the interest paid by banks to borrow money from the Federal Reserve Bank. Interest is, basically, the cost to the banks of borrowing someone else’s money. The banks will pass on this cost to their own borrowers.

As a way to boost the economy, remember that the Fed set its benchmark interest rate close to zero in late 2008 and did the same thing at the beginning of the COVID pandemic. This resulted in “free money.”

By reducing the federal funds rate, the Fed increased the supply of money by making it less expensive to obtain. As a result, businesses could have greater access to money. They could spend more on building their businesses and on hiring more employees. Because consumers and businesses had more money, they could purchase more goods, services, houses, and stocks.

Increasing the federal funds rate, on the other hand, reduces the supply of money by making it more expensive to obtain. Reducing the amount of money in circulation, by decreasing consumer and business spending, helps to reduce inflation. However, the Federal Reserve has to decide whether the increase in consumer demand and in hiring has led to enough inflation in prices to warrant a reduction in rates.

Consequences for Consumers and Businesses

Any increased expense for the banks to borrow money has a ripple effect, which influences both individuals and businesses in their costs and plans.

Effect on individuals – Banks increase the rates that they charge to individuals to borrow money, through increases to credit card and mortgage interest rates. As a result, consumers have less money to spend. They must face the effect on what they want to purchase and when to do so.

Effect on business – Because consumers have less disposable income, businesses must consider the effects to their revenues and profits. Businesses also face the effect of the greater expenses of borrowing money. As the banks make borrowing more expensive for businesses, companies are likely to reduce their spending. Less business spending and capital investment can slow the growth of the economy, decreasing business profits.

These broad interactions can play out in numerous ways.

Special Effects

The stock market as a whole – Stock prices decrease when investors see companies reduce growth spending or make less profit. Absent other economic effects, the value of stocks in general will fall.

Bond market – As the stock market drops, investors tend to view the risk of stock investments as outweighing the rewards. They will often move toward the safer bonds and Treasury bills. As a result, bond interest rates will generally rise, and investors will likely earn more from bonds.

The dollar – When other central banks are expanding the money supply, it weakens the value of their currencies. If the Fed hikes the interest rate, then the dollar appreciates. A stronger dollar means that U.S. consumers pay less for imports. A stronger dollar will boost U.S. demand for products from Asia and Europe, which will increase corporate profits there. As a result, global stocks will likely increase in value.

Commodity prices – A stronger dollar has often contributed to the reduction in oil prices in the past year. As the dollar could become even stronger with the reduction of interest rates, the prices of commodities, especially oil, should decrease. And often the opposite is true. Of course, investments in oil stocks will likely also lose some value.

The federal budget – The U.S. government has a very large debt, and increased interest rates lead to higher interest payments.

Corporate borrowers – Companies that are repaying loans will end up with higher interest payments.

Mortgage holders – Payments on mortgage interest will increase for individuals and companies whose mortgages do not carry a fixed interest rate.

Obviously, many factors affect activity in various parts of the economy. A change in interest rates, although important, is just one of those factors.

The Fed’s Next Timing

The Federal Open Market Committee, which sets the rates, will meet again three more times before next year, starting on:

- September 20-21

- November 1-2

- December 13-14

While there are expectations that more rate hikes are coming in 2022, circle these dates on your calendar and expect to hear lots of chatter.

And while many factors can affect the market, it is important to prepare for any effects on your business, your livelihood, and your investment portfolio when an increase in the federal funds rate does take place.

Be sure to talk to your financial advisor for specific guidance.

Copyright © 2022 FMeX.