Retirement planning is a primary reason for long-term saving, and when people think about retirement, finances are often the focus. However, it is important to also look at the non financial aspects of transitioning from the world of work to the world of leisure. Specifically, lifestyle changes and self esteem issues associated with the loss of your professional identity may create difficulties. As you’re preparing strategies for your future well-being, give some thought to the kind of retirement you envision for yourself.

Consider the following questions:

- What do you find fulfilling?

- What gets you out of bed in the morning?

- What are your strengths and weaknesses?

- Do you work well as part of a team, or do you thrive on solitude?

- Do you have a lot of physical energy, or do you prefer a more sedentary pace?

- Do you have a hobby you always wanted more time to pursue?

Don’t be afraid to think outside the box. This informal self-inventory may hold the key to your vision for retirement.

Challenging Conventions

The concept of retirement in America is changing. Traditionally, retirement has been idealized as a leisurely phase of life, a reward for the many years of working and raising children. This concept is based on the assumptions that people will enjoy themselves in retirement, and that work, as we commonly know it, is the province of younger generations.

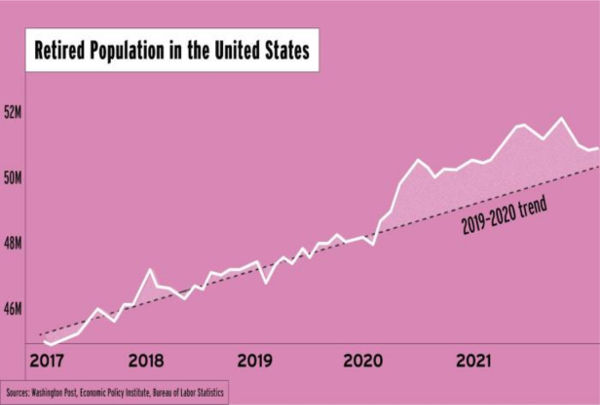

However, is this concept realistic for those of us still years away from retirement, and if it is, is it what we really want? The answer might surprise you. Especially when you learn that by early 2022, roughly 1 million U.S. retirees had reentered the workforce. Now, it’s true that many retirees reentering the workforce had no choice, but for others the choice was intentional.

Rethinking retirement means reexamining conventional ideals to determine whether they apply to today’s reality and what we envision for ourselves.

Intrinsic to the conventional notion of retirement are significant assumptions about work, money, and retirement standards of living. For previous generations, work was thought to be something you did for about 45 years (until roughly age 65), and then, suddenly, you never had to (or wanted to) work again. A company pension, Social Security, and some savings generally provided enough income for funding a comfortable lifestyle in retirement, including leisure, travel, and recreation.

If that’s what you want for your retirement, there is nothing wrong with pursuing that goal. However, for some, work is too much a part of their sense of “self” to be suddenly cast aside. Moreover, with so much of their daily lives centered around work, some people have difficulty imagining their life without that structure.

Furthermore, changes in employer-sponsored retirement plans (i.e., the decline of defined benefit plans and the rise of defined contribution plans) have altered our expectations about retirement funding. The responsibility has shifted from employer to employee, which means that an individual’s long-term saving for retirement must now be factored in with other savings objectives, like purchasing a house or funding a college education for children, and ongoing financial responsibilities.

Finally, the traditional concept of retirement is based on the belief that one’s standard of living will be sustainable in retirement, and it may be for some. For others, however, it may be more practical to ask what standard of living can be maintained based on projected resources. This type of approach might help you see what is realistic (and what may be unrealistic) in your situation, and it may help you set more realistic retirement priorities. For some people, downsizing their standard of living in retirement may be acceptable. For others, however, maintaining the same standard of living during retirement as during their working years may be the goal.

Consider Phased Retirement

As you consider the traditional concept of retirement, you may discover that it doesn’t meet your needs. Phased retirement is a term coined to describe a range of employment arrangements that allow an employee who is approaching retirement to continue working, usually with a reduced workload, in transition from full-time work to full-time retirement.

Many individuals may want to continue some form of work, such as consulting, job-sharing, mentoring, or providing back-up management. Mentoring, in particular, enables an individual to transfer a lifetime of learning and experience to a friend, relative, or younger colleague. Aside from money earned from continued work, phased retirement may help you maintain a feeling of involvement in the world and may provide a sense of purpose.

For some, phased retirement may be an option. For others, it may be a necessity. For still others, phased retirement may provide structure to daily life and the opportunity to explore other activities while maintaining a meaningful role within an organization, the community, or society in general.

What’s most important, however, is to define your vision of retirement in a way that makes sense to you and is realistic considering your goals and resources.

Copyright © 2022 FMeX.