Things to think about as you review your long-term retirement strategy

Tempted to stash your money in a bank CD? Or maybe under your mattress? Think either one of them will keep pace with inflation? Think again.

Inflation

Inflation is defined as an increase in the general level of prices for goods and services. Deflation, on the other hand, is defined as a decrease in the general level of prices for goods and services. If inflation is high, at say 10% – as it was in the 1970s – then a loaf of bread that costs $1 this year will cost $1.10 the next year.

Currently, the inflation rate in the US is very high. Historically, inflation in the US has averaged 3.3% from 1914 until 2021, but it reached an all-time high of 23.7% in June 1920 and a record low of -15.8% in June 1921.

So how does inflation affect your retirement savings? The answer is simple: inflation decreases the purchasing power of your money in the future. Consider this: at 3% inflation, $100 today will be worth $67.30 in 20 years – a loss of 1/3 its value. Said another way, that same $100 will only buy you $67.30 worth of goods and services in 20 years. And in 35 years? Well your $100 will be reduced to just $34.44.

Bank CDs

A certificate of deposit – a CD – is what’s known as a time deposit account – a bank agrees to pay interest at a certain rate if savers deposit their cash for a set period of time. Generally speaking, the interest rate paid by the bank increases as the term (the length of time the bank has your money) increases. CDs are also insured by the Federal Deposit Insurance Corporation for banks and by the National Credit Union Administration for credit unions.

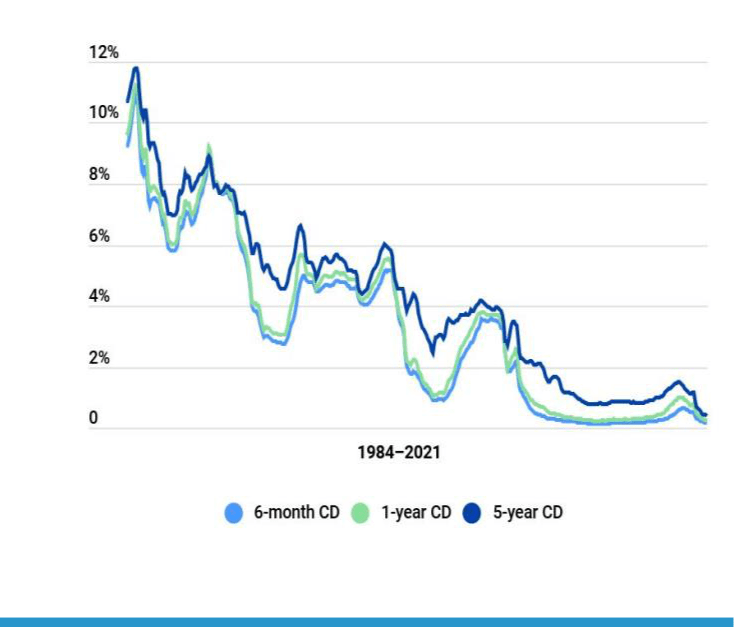

As the chart below shows, CD-yields have been in a steady decline for the past 35+ years:

More specifically, compare three dates from 1984, 2017 and 2022 to see the disparity:

| July 3, 1984 | January 6, 2017 | January 13, 2022 | |

|---|---|---|---|

| 1-year CD yield | 11.27% | 0.27% | 0.14% |

| 5-year CD yield | 12.06% | 0.86% | 0.26% |

The Mattress

Surprisingly, we all know people who prefer to keep their savings under a mattress or in a shoe-box hidden away in a closet. But here is what a world-renowned study of every investor who hid their money under a mattress or in a shoe-box found:

| Avg. Annual Returns | Mattress | Shoe-Box |

|---|---|---|

| Last 5-years | 0.0% | 0.0% |

| Last 25-years | 0.0% | 0.0% |

| Last 100-years | 0.0% | 0.0% |

Unfortunately, there was not enough data going back more than 100-years, but I suspect the returns would have been the same.

The Stock Market

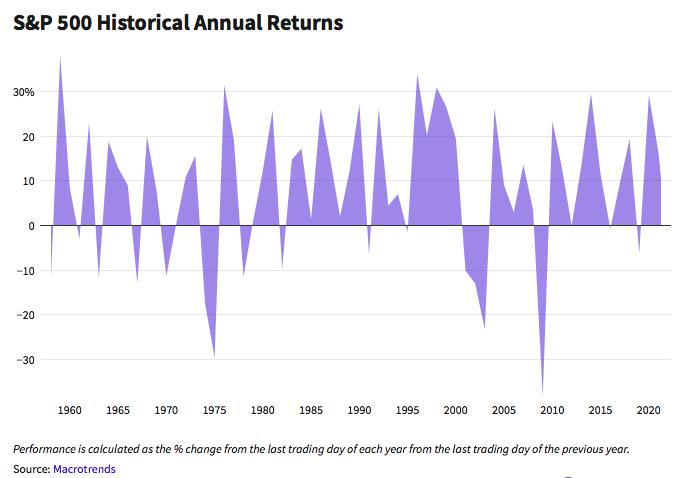

If you are looking for average stock market returns over a long period of time, you are likely to get different numbers from different sources. This is because your answer really depends on a number of variables, including which index you review, whether dividends are included or not, whether the effects of inflation are calculated, etc.

Most financial professionals would agree, however, that the long-term data for the stock market points to an average annual return of about 10%. In fact, the S&P 500 has returned a historic annualized average return of 10.5% since its 1957 inception through 2021.

And let’s not forget what 2021 brought investors:

• The DJIA rose 18.7% in 2021;

• The S&P 500 rose 26.9% in 2021;

• NASDAQ rose 21.4% in 2021; and

• The Russell 2000 Index rose 13.7% in 2021.

What Investors Need to Remember

Although there are times when buying a CD might be appropriate, generally speaking, buying CDs should not be part of your long-term retirement strategy – unless you happen to be very close to retirement age. CD rates today just don’t keep pace with inflation. And putting your money under a mattress is worse (and probably uncomfortable too).

Instead, I encourage you to explore the thousands of financial products that provide better options. And remember that over long-periods of time, the stock market has outpaced inflation, today’s CD yields and hiding your money under your mattress.

But before you invest in anything, consider the risk/reward tradeoff, your goals and your time horizon

– and call our office to discuss.

Copyright © 2022 FMeX.